Loan-to-Value Ratio: How the LTV Ratio Affects Homebuyers

Written by MasterClass

Last updated: Feb 4, 2022 • 5 min read

If you're a new homebuyer, applying for your first mortgage may seem like a complex and daunting task. To prepare yourself for this important life step and increase the chance of securing an approved loan, it's essential to understand the intricacies of LTV ratios.

Learn From the Best

What Is a Loan-to-Value (LTV) Ratio?

A loan-to-value ratio (LTV ratio) is a number used by mortgage lenders to assess the risk of loaning money to a borrower before they approve a real estate mortgage. The LTV ratio depicts the ratio between the value of your home loan and the purchase price or appraised value of your home (whichever amount is less). Your LTV ratio is an important factor in determining if a lender will approve a certain loan amount, and it also affects your minimum down-payment. A lower LTV ratio will increase your chance of mortgage loan approval and give you more favorable loan terms.

Why Is Understanding LTV Ratios Important?

While LTV ratio isn't the only factor a lender's underwriting department considers when evaluating a loan, it's a critical one. Whether you're buying your first mortgage or refinancing an existing mortgage, a lender will always look at your LTV ratio. It’s important to understand what this number means and optimize it for the following reasons.

- 1. LTV ratio affects your interest rate. In general, a lower LTV ratio means you'll receive a lower interest rate. If your LTV ratio is eighty percent or lower, lenders will typically offer you the lowest possible interest rate. If you have a high LTV ratio, such as ninety percent, a lender may still approve your loan but with a higher interest rate.

- 2. LTV ratio helps you determine your down payment. If you request a loan that's similar to your home's appraised market value, it creates a higher LTV ratio and signals to lenders that it's a risky loan to approve. The reason? You barely have any equity in the home, meaning that there's a higher chance of defaulting on the loan and it will be difficult for the lender to profit off the sale of the home in the event of a foreclosure. In order to obtain a good LTV ratio and incentivize the bank to approve your loan, you can increase your down payment on the house. Increasing your down payment simultaneously increases your equity in the home and decreases the amount of money you need to borrow.

- 3. LTV ratio influences whether you need private mortgage insurance (PMI). Practically every lender will require you to purchase PMI if your LTV ratio is higher than eighty percent. The purpose of PMI is to protect the lender in the event that you stop making monthly payments on your loan. If your lender requires you to have PMI, you'll typically pay an extra PMI premium that's added to your monthly mortgage payment. To avoid this extra cost, do your best to make your LTV ratio eighty percent or lower.

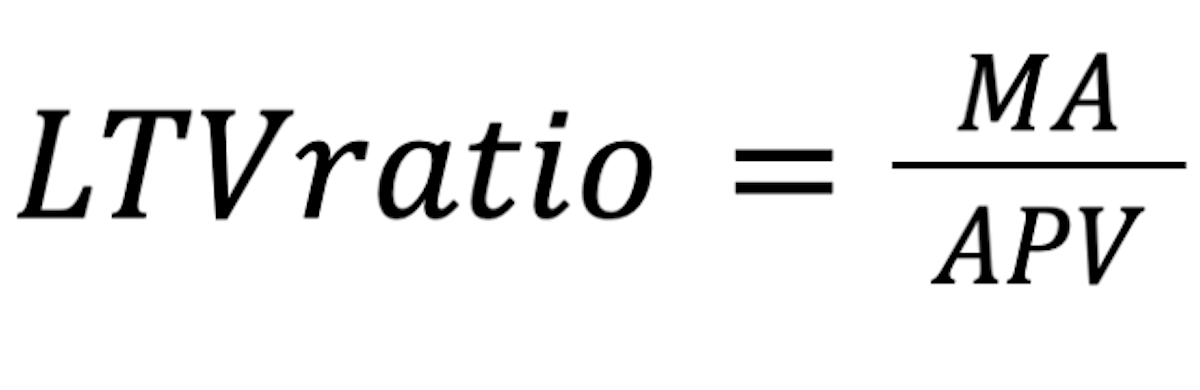

How to Calculate LTV Ratio?

You don't need to know advanced math to calculate your LTV ratio. All you need to know is the amount of your mortgage loan, the appraised value of the property, and the following formula—

—where “MA” is the mortgage amount and “APV” is the appraised property value.

For example, if you purchase a home appraised at $500,000 and pay a $75,000 down payment, that means you'll need to request a mortgage loan of $425,000 to cover the rest of the cost. To calculate LTV ratio, just divide $425,000 by $500,000 and you'll end up with an LTV ratio of 85 percent.

While it's common for the appraised property value to equal the purchase price, this isn't always the case. In the event that the appraised value and purchase price are not the same, it's important to know that a lender will calculate LTV using the lesser of the two numbers. This means if you purchase a property for more than its appraised value, your LTV ratio will increase.

How to Lower Your LTV Ratio

There are only two ways that you can lower your LTV ratio. The first is to find a cheaper property to purchase. The second is to save up more money and make a larger down payment so you don't need to borrow as much money.

LTV Ratio Requirements for 4 Different Loan Types

The ideal LTV ratio varies depending on the lender and type of loan.

- 1. Conventional loans. The ideal LTV ratio for a conventional loan is eighty percent or less, meaning you'll need to make a down payment of at least twenty percent. If you hit this target, you can most likely receive a low interest rate and avoid paying private mortgage insurance.

- 2. FHA loans. These mortgage loans are insured by the Federal Housing Administration and are popular with lower income first-time homebuyers. FHA loans require a lower credit score and minimum down payment than most conventional loans. Lenders will generally approve FHA loans with a LTV ratio as high as 96.5 percent, but you will need to pay for mortgage insurance for the lifetime of the loan no matter how low your LTV ratio drops over time. Due to this caveat, it's common practice to refinance the loan once your LTV ratio hits eighty percent in order to remove the mortgage insurance requirement.

- 3. USDA loans. The U.S. Department of Agriculture offers these loans to lower income homebuyers in rural areas and will approve loans with a LTV ratio as high as one hundred percent if you meet certain additional requirements.

- 4. VA loans. The U.S. Department of Veterans Affairs offers these loans to veterans and current military members. You can obtain a VA loan with an LTV ratio as high as one hundred percent as long as you meet certain additional requirements.

What's a Combined LTV (CLTV) Ratio?

Unlike an LTV ratio which only examines one mortgage balance to make a risk assessment, a combined loan-to-value ratio (CLTV ratio) incorporates additional secured loans into the assessment. In addition to a homeowner's first mortgage, CLTV ratios can include a second mortgage, home equity loan, or home equity line of credit (HELOC). The purpose of a CLTV ratio is for lenders to accurately assess a prospective homebuyer's risk of defaulting when the homebuyer is taking out more than one loan or line of credit.

Ready to Learn the Ins and Outs of the American Housing Market?

All you need is a MasterClass Annual Membership and our exclusive video lessons from prolific entrepreneur Robert Reffkin, the founder and CEO of the real estate technology company Compass. With Robert’s help, you’ll learn all about the intricacies of buying a home, from securing a mortgage to hiring an agent to tips for putting your own place on the market.